The media labels it a Banking Royal Commission, continuing the terminology adopted in calls for an inquiry over the last few years, but the Terms of Reference are much broader. Not only do the requirements focus on both superannuation (and wealth management and financial advice) and insurance, but there are curious inclusions and exclusions. It's difficult to see whether much can be achieved in the relatively brief time available to report.

Amid the flurry of both praise and criticism of the Commission, former Reserve Bank Governor and Treasury Secretary (and more recently, industry super board member), Bernie Fraser, was an example of the widespread concern. He has seen decades of such inquiries, and he said:

"You shouldn't prejudge these things of course but I don't think this sort of politically-motivated Royal Commission is going to make any significant progress."

I have had reservations in the past, such as in this article on 10 reasons not to hold a bank royal commission. We ran a reader survey a year ago and 70% of respondents opposed the idea.

None of this matters much now as the decision to proceed has been made. What can we expect when the Commission reports in early 2019?

Banks dodge some of the bullets

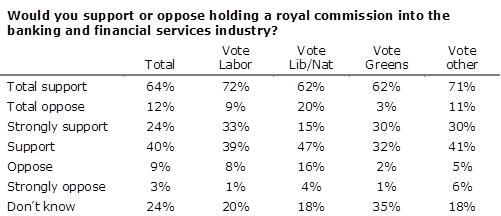

The people calling for a Royal Commission into the banks were no doubt celebrating Malcolm Turnbull's policy reversal, even labelling it a 'bankflip'. The Guardian Essential Report showed two-thirds of voters support a 'banking inquiry'. But would the strong populist support have been directed at a super inquiry? It was not mentioned in the survey question:

Source: The Guardian Essential Report, 28 November 2017

A closer read of the Terms of Reference reveals there might be some quiet satisfaction in the corridors of bank senior executives after they took the gamble to accept the inevitable. The bank chairs and CEOs decided to encourage the government to hold a royal commission, saying "it is now in the national interest for the political uncertainty to end". They felt it was better to have an inquiry where a reluctant Prime Minister and Treasurer set the rules rather than a rabid coalition of Greens and Labor.

The banks will be pleased by the broad focus on financial services. The inquiry is called a "Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry." In fact, the Terms of Reference refer to financial services far more than banks, and the text is littered with superannuation directives, such as ensuring large super funds are caught in the definitions:

"an RSE licensee of a registrable superannuation entity (as that term is defined in the Superannuation Industry (Supervision) Act 1993)."

If you want to know more about RSEs, check the APRA website. SMSFs are not RSEs.

Perhaps the most controversial reference says the Commission must inquire into:

"the use by a financial services entity of superannuation members’ retirement savings for any purpose that does not meet community standards and expectations or is otherwise not in the best interest of members."

The politics are inescapable. The Government, led by Financial Services Minister Kelly O'Dwyer, has been targetting governance and board composition in the industry fund sector, and use of member funds brings fund governance to the fore and will partly distract attention from the banks. O'Dwyer told the Association of Superannuation Funds of Australia (ASFA) Conference the day after the Commission was announced:

"It is disappointing that some industry participants have used members' money in a multimillion dollar advertising campaign and lobbying effort to defeat increased transparency and accountability in the sector. One can only wonder why."

Industry reacts according to impact

Within hours of the announcement of the Royal Commission, media releases and comments from industry participants hit the newsrooms. ASFA, the peak body representing the large super funds, said:

"ASFA is disappointed the Government has included superannuation in the scope of the Royal Commission. A plethora of never ending inquiries, reviews and regulation is at odds with maintaining a system that is serving Australians tremendously well."

Meanwhile, the SMSF Association was pleased to see its sector excluded from the terms of reference, and CEO John Maroney advised:

"A Royal Commission into banking and financial services will provide an opportunity to increase transparency and improve ethics and professionalism across the financial services sector."

At the Australian Institute of Superannuation Trustees (AIST), CEO Eva Scheerlinck said:

"We think this is ideological. It is an extension of the Royal Commission into the unions, where the government probably didn't get the results it wanted. It is another attempt at getting at the unions through the super model."

Former Victorian Premier and now Chair of CBus Super Australia (an industry fund), Steve Bracks, told the ASFA Conference:

"Australia's super system is world class, and there is no evidence of gouging, fraud or unethical behaviour to warrant a Royal Commission into the industry. I don't think the Government necessarily has an axe to grind against superannuation. I think they are using superannuation as the prism to get something else. Clearly, there is an ideological agenda there, not a commitment to really fundamentally change the system, but to break the model so they can get at the equal representation and trade union involvement in superannuation funds."

The super industry has already demonstrated that 2018 will be filled with public debate on issues the average person saving for retirement neither knows nor cares about.

Implications for investing

The biggest cost is not the estimated $75 million expense of the Commission itself. It is the massive distraction across the entire financial services sector, forcing executives to respond every day to new claims and accusations rather than running their businesses. Imagine the hundreds of millions of dollars spent on committees, meetings, consultants, lawyers, advisers and the thousands of people who will spend most of 2018 managing the fallout. Many of the Commission's issues will be populist, trivial and borderline irrelevant, but resources will be thrown at them on an enormous scale. The incoming CEO at CBA will have an overwhelming distraction when he or she should be focussing on improving the efficiency and management of the bank. It will paralyse innovation at a time of new competitive forces, especially from fintechs and global platforms, who will be given an easy ride through the morass.

Regardless of what the Commission finds, banks will become more conservative, compliance departments will expand rapidly and risk aversion will increase. There will be even more focus on the core activity of borrowing and lending and less on areas where banks have brought capital and innovation, such as in wealth management.

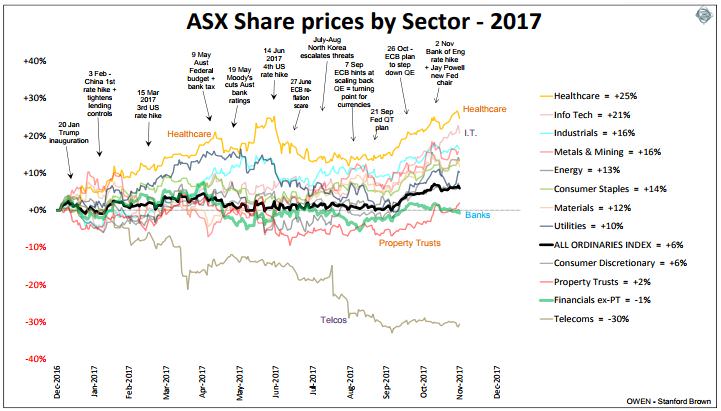

In 2017, the finance sector has already been a major drag (with Telstra) on the Australian market, contributing to the S&P/ASX300 Index underperforming foreign markets such as the S&P500. Admittedly, the bank scandals have contributed to this malaise, but the days of double digit earnings growth and rising dividends are over. As shown below, Financials and Telecoms are the worst sectors in 2017.

Click to enlarge

Against this backdrop of struggling growth, bankers should be banking, but instead they'll be reacting. And throughout 2018, executives and board members will file through the doors of the Commission to be interrogated like naughty children, and the media will serve up a nightly diet of undermining stories.

What can we expect from these Terms of Reference?

Yes, the banks deserve much of the criticism (see my book, Naked Among Cannibals, for example), but let's look deeper into the woolly Terms of Reference. There is this curious directive:

"The Commission is not required to inquire into, and may not make recommendations in relation to macro-prudential policy, regulation or oversight."

What is macro-prudential policy? It is defined as: "policy and regulation ... concerned with containing systemic risk, which can have widespread implications for the financial system as a whole, beyond simply the banking system."

This seems to instruct the Commission not to inquire into matters which have widespread implications for the financial system. Strange. And what does "beyond simply the banking system" mean?

What will the Commissioner, former High Court Judge Kenneth Hayne, make of the directive to study:

"the particular culture and governance practices of a financial services entity or broader cultural or governance practices in the industry", and

"any conduct, practices, behaviour or business activity by a financial services entity that falls below community standards and expectations."

What can the Commission realistically recommend? What rules can govern culture? ASIC said recently:

"Culture is not something we want to regulate with black letter law ... It is an issue companies themselves must address."

And whose community standards? Most Australians benefit from healthy bank profits via their superannuation. It was only two weeks ago that Malcolm Turnbull told Channel Nine’s Today show that a Royal Commission “doesn’t do anything other than write a report”.

Let me guess at the conclusions: there should be better regulatory oversight, an improved compliance regime and a recognition of the multiple needs of stakeholders. There, that should fix it.

Graham Hand is Managing Editor of Cuffelinks.