The proposed superannuation changes generated the full range of emotions, from outrage to praise. The comments among the 700 responses reveal as much as the overall scores. The survey was reported widely in the media, showing the extent of interest in reactions to the proposals.

For a full range of comments, see also the article on retrospectivity and the article on how future large balances will be limited.

At one extreme supporting the proposed changes, responses in the survey and the articles argue the current tax concessions are too generous and unsustainable, and the proposals still mean superannuation retains its benefits. At the other extreme, readers are upset about broken promises (from both sides of politics), even suggesting this is a vote changer for them. And everything in between.

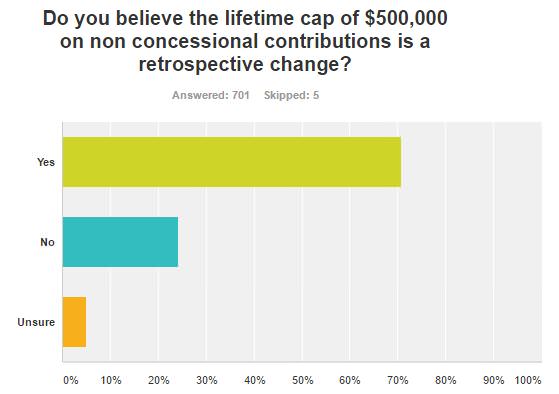

On the question of retrospectivity of changes, over 70% of respondents believe the proposed non concessional cap is a retrospective change.

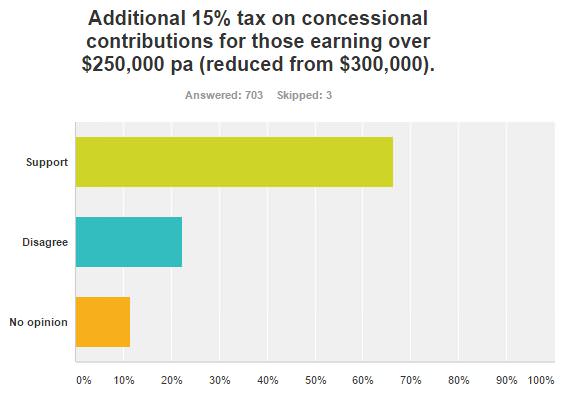

But illustrating that the survey results were not simply about preserving benefits for the wealthy, a solid 66% supported the reduction in the threshold where the additional 15% tax on concessional contributions applies.

Answers to all 12 questions are available by clicking the link above.