As a rational value investor, it makes sense to buy an asset at a price less than the tangible value of the asset with an expectation that over time, the value will be realised. Listed Investment Companies (LICs) trading at discounts to their net tangible assets per share (NTA) may present a value opportunity but if these discounts persist over time, then this value may never be released. Some LICs remain at a discount to their NTA for years.

Here is a very simple illustration of a discount and premium to NTA.

You have $10,000 to invest in the stock market and you’ve decided to use a LIC to gain exposure to a particular equities strategy.

LIC opportunity 1 with discount to NTA

LIC 1 offers a basket of listed stocks, and 10,000 shares with an underlying market value of $10,000 and NTA of $1 per share are available for a 10% discount of 90 cents. You pay $9,000 for $10,000 worth of underlying stocks.

LIC opportunity 2 with premium to NTA

LIC 2 offers a basket of listed stocks, and 10,000 shares with an underlying market value of $10,000 and NTA of $1 per share are available for a 10% premium of $1.10. You pay $11,000 for $10,000 worth of underlying stocks.

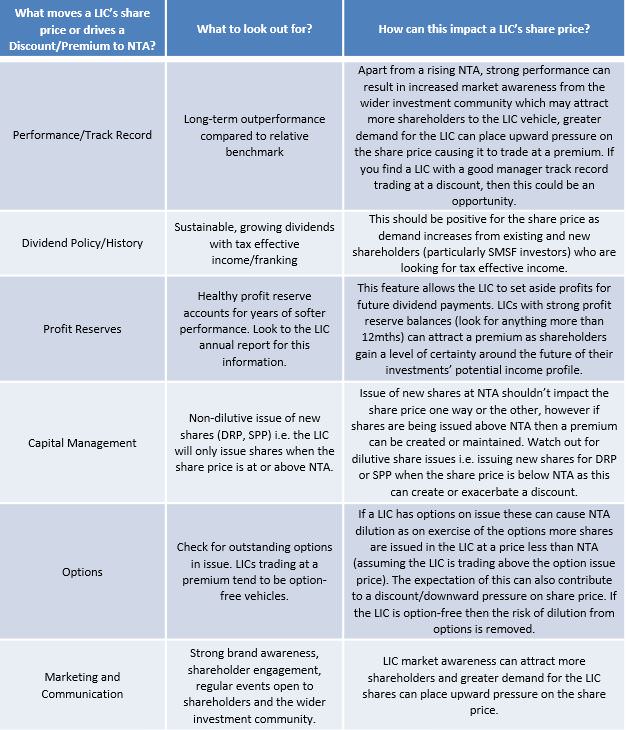

What causes this disparity?

These differences occur despite the NTA being readily identifiable from the issuer’s website or ASX announcements.

For example, a LIC premium to NTA can exist when there is a lot of demand for the LIC for various reasons, or if the company is issuing more shares at a price greater than the NTA. However, if there is little demand for a LIC, selling activity can place downward pressure on the share price causing it to trade at a discount. If a company issues more shares at a share price lower than the NTA, this can further exaggerate the discount. The management and boards of LIC need to closely watch the relationship between NTA and the price of new shares.

On first look, it seems the rational investor could take advantage of the discount opportunity, but the following is a list of the key items investors should consider to gauge whether a LIC trading at a discount could move towards trading at NTA or even a premium.

It’s not an exact science but in our view, a LIC trading at a discount exhibiting many of the positive attributes mentioned above could present an opportunity to unlock value via the narrowing of the discount over time.

Julia Stanistreet is a Business Development Manager at NAOS Asset Management. This content has been prepared without taking account of the objectives, financial situation or needs of any individual. It does not constitute formal advice.